B2B platforms need to have a financial services strategy

"The Internet? Is that thing still around?"

— Homer Simpson

The internet is a great enabler for software to take over the world. Over time, B2B internet software business models have evolved in distinct phases. In today’s market, buyers and sellers have more ways to communicate with each other than ever before.

Version 1.0 of commerce on the internet was about removing information asymmetry and lowering search costs. In the pre-internet world, buyers and sellers found each other through offline distribution channels using traditional modes of communication, including newspapers, phone books, radio, word-of-mouth, and direct face-to-face sales. Then, the internet changed everything. Buyers and sellers were able to connect more efficiently and cheaply than through the traditional channels. Suddenly, a whole world of communication possibilities opened up, which companies like Amazon and eBay took advantage of and grew exponentially. They were the defining companies in Version 1.0

As the internet and, more importantly, software became a central part of consumers' and businesses' daily lives, Version 2.0 took shape. Version 2.0 was about building horizontal workflows delivered via cloud-based software to help a business scale its internal operations. Asa result, Version 2.0 led to category-defining companies such as Salesforce (sales and marketing)and Intuit (accounting). The companies in this wave focused on solving the horizontal problems that affected every company.

Fast forward to the last few years, software continued to eat the world and started penetrating niche verticals. Version 3.0 is about the rise of the B2B SaaS, i.e., vertical niche software. This wave saw the rise of Procore (construction), Toast (restaurant POS), and many more niche B2B companies. Companies in this wave have a vertical focus. They stick to one vertical and go deep into its specific problems. These companies want to be a one-stop shop for customers in their vertical. Now, B2B SaaS is the dominant software model and is proliferating..

The flip side of this explosive growth in software dominance shows that the cost of making software and launching this product is dropping rapidly. This cost decrease has in turn caused an increase of competition in almost every B2B category. As a result, differentiation between software products’ features and pricing has become more difficult. Almost every product feature can be replicated easily. Pricing is now a race to the bottom—who can make it the cheapest and sell for less than their competitors.

Consumer businesses have a solution to this problem using the ads business model. The core product is offered for free and the ads make money for the company. This model enables businesses to compete on purely product features. Winning becomes an execution-,innovation-, and luck-based game. Price is completely taken out of the equation. However, this model has its challenges. The incentives between the company and the end-user are not aligned. An ad-supported business model in B2B seems implausible. It will be tough for business users to buy into an ad-supported model to generate revenue

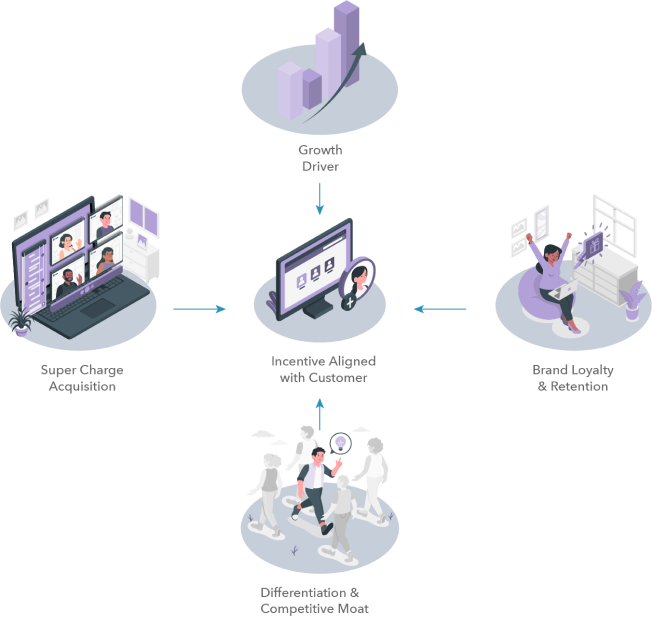

However, incorporating financial services into B2B software products offers an incentive-aligned solution. Business customers have financial needs and they are often willing to pay for easy and convenient access to financial services. Software platforms have a unique data advantage. They know a lot about their customers' business activities through data collection and can use this intel to build magical experiences for their customers. This method of monetizing through financial services is a customer-aligned model since customers are getting real value in exchange for their data. Whereas with the ad-supported model, most of the value accrues to the platform and all the user gets is product utility. In the financial services supported model, the customer receives product and economic utilities. The software platform can then offer its core product for free and thus removes price out of the equation. It can compete entirely on product value, which in turn accrues value back to the customer

The financial-services model is a completely aligned incentive model. Customers come for the free software and stay for the financial services, leading to a supercharged acquisition model that is competitive and rewarding to businesses.

It's hard to compete against free.

Evolution of B2B SAAS

Customer preferences have also evolved significantly. Customers envisage a simplified UX, a high degree of automation, and tailored experiences for their needs. Customers expect vertical software players to solve their problems end-to-end. Financial services, i.e., anything and everything to do with money, is a core need in any business. Customers will need to manage all aspects of cash transactions with the software they use daily. B2B software can offer customers a single place to go and a complete operating system for your business. This promise is incomplete without financial services. In the past, it was understandable that financial services were not on the core product roadmap. Rather, it was a complicated and regulated business, but the landscape has since changed. Fintech software now provides concise operations that enable non-fintech companies to develop and deploy financial services to their customers easily

Financial services are also an effective Gross Merchandise Value (GMV) growth driver.Businesses thrive on capital, which is the primary fuel that makes businesses tick. The more you can help your customers grow, the more they will spend and transact on your platform. The more they grow, the more you grow as a result, which is the ultimate growth loop.

Growth Flywheel

Customer retention and brand loyalty are the holy grails of any business. Financial services provide another mechanism to accelerate these goals. By providing a complete suite of products that includes financial services, software platforms can differentiate themselves from the competition. They can fulfill the brand promise of: "We solve all your problems, in one integrated offering." This platform creates incredible product and brand loyalty. Why would a customer ever choose a piecemeal solution over a slick integrated offering?

It's hard to compete against free.

Offering financial services to your customers is the next evolution in the B2B SaaS business model. Build product differentiation, supercharge your acquisition, increase your retention, and in the process, give your users what they want!

Kanmon is operated by Kanmon Inc. Kanmon Inc makes capital available to businesses through business loans, lines of credit, and advances. California loans are made pursuant to Kanmon’s California Department of Financial Protection and Innovation (DFPI) Finance Lenders Law License #60DBO-144925. Kanmon does not currently meet the applicability thresholds for the California Consumer Privacy Act. As set forth in our Privacy Policy and with respect of California residents, Kanmon will not share information we collect about you with affiliated or non-affiliated third parties, except in the limited circumstances disclosed in our Privacy Policy and permitted under California law, or if you give us permission. To learn more, please contact hello@kanmon.com.