Your customers want access to capital – why not give it to them

Businesses are the lifeblood of the economy. They employ people, provide critical public funding in the form of tax dollars, and help improve prosperity nationwide.

As businesses grow, communities grow with them. Thus, any improvement in the private sector can ripple out to significantly increase overall economic wellbeing. As a result, helping businesses grow is in the best interests of everyone. But what are some of the most common challenges businesses face as they scale? Read more to find out.

What are the key challenges to growing a business?

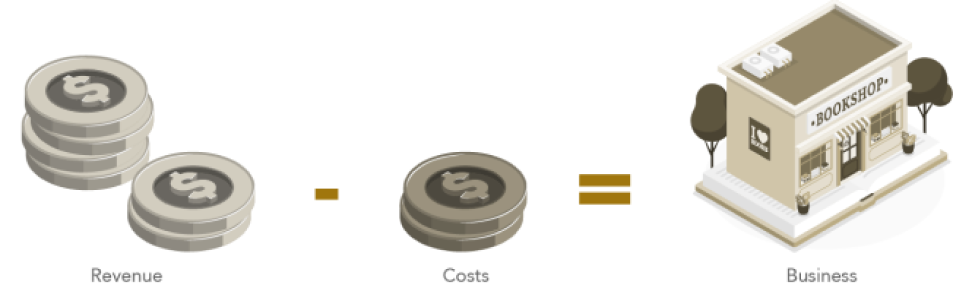

Companies survive by providing value for their customers. In return, customers pay money for the value they receive. To grow, a business must ensure that the cost of delivering the value is less than the value it provides to the customer. Or in other words: businesses grow based on the difference between revenues and costs.

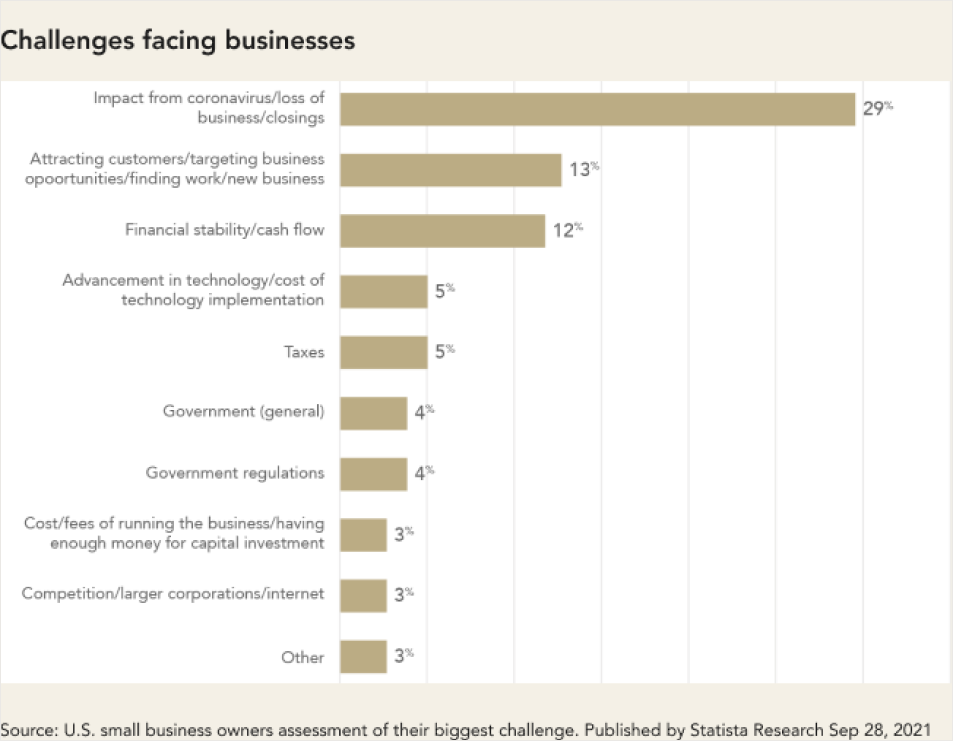

These challenges are evident in the data in 2021. According to the recent Statista Research survey, the top three challenges for businesses were boiled down to:

This is the basic framework – but achieving this model is easier said than done. Over time, the main business challenges have been consistent:

Can I find enough customers in a cost-efficient way?

If you don’t have customers, you don’t have a business. But you can’t spend all of your revenues on acquiring new customers. So, growth requires acquiring customers cost-efficiently – after all, revenue must always be lower than costs.

Can I produce a product that customers will pay for?

If customers don't see any value in your product, they will not pay for it. No revenue = No business.

Do I have enough cash for start-up as well as ongoing operations?

Depending on your business, some initial startup costs can be quite significant. Specialized equipment and labor, for example, can really rack up a price tag. Even worse, all this money must be spent before a single cent of revenue is produced.Creating a marketable product does not happen overnight. There may be a significant amount of time required to develop a product and then selling it to the customer. As a result, there is always a need for working capital in any business.

Cash is the fuel that makes business possible.

Cash is always in short supply and in high demand.

These challenges are evident in the data in 2021. According to the recent Statista Research survey, the top three challenges for businesses were boiled down to:

- The impact of COVID,

- Difficulty finding customers, and

- Access to capital

Access to capital has been the most acute challenge, particularly as the world economy adapts to the new normal in the post-pandemic world. Whether a business has funding or not is a major determination in whether it will be able to manager downturns and, most importantly, beset up for success for the eventual boom that comes after. In the post-COVID recovery, companies with access to capital perform significantly better as they can quickly scale up production and hire talent to meet the significantly increased demand. But what type of capital are businesses looking for – and how do they find it?

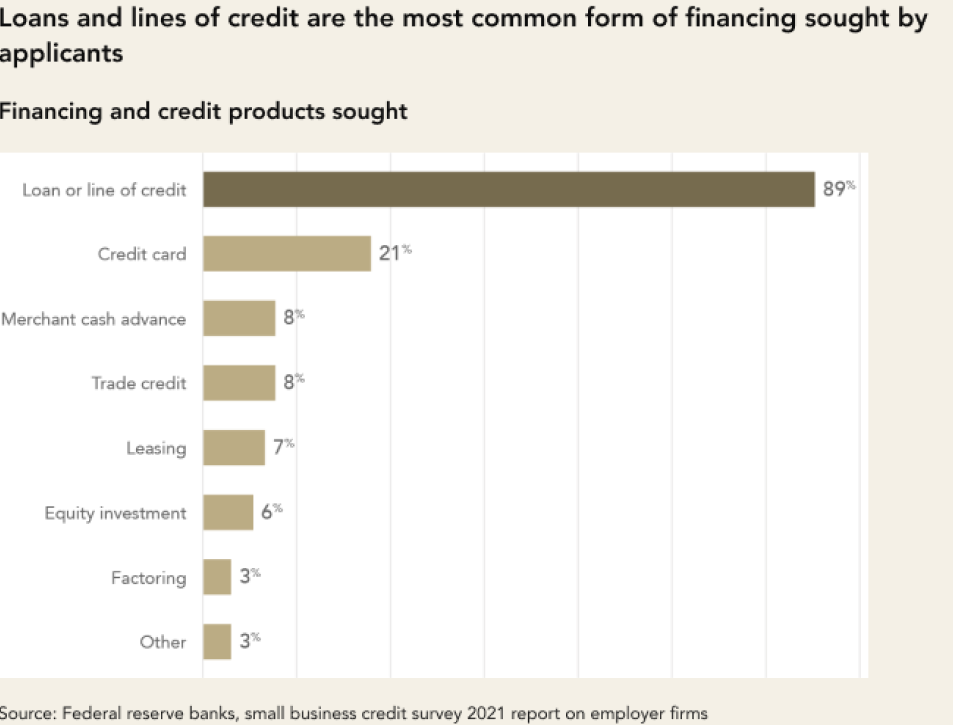

What type of capital are businesses looking for?

The data tells a straightforward story: the overwhelming majority of financing requests are for term loans or lines of credit.

To understand why, view it from the perspective of a business owner. The critical criteria business owners typically use to evaluate financing options are whether they can get a significant amount and how much the capital will cost.

Is the capital amount significant enough?

Owners want to have access amounts of capital sufficient to fund their operations for at least several months. Having access to capital gives business owners peace of mind. With working capital, the larger the buffer, the greater the ability to respond quickly to changes in demand and opportunistic revenue growth. Therefore, large loan amounts matter.

How much does it cost?

Going back to the basic equation for business: Value = Revenue – Cost. A savvy business owner is always looking for the best bang for her buck. Thus, the cost of financing is a major consideration, as do the repayment terms.

Can I budget for capital costs predictably?

Owners want payment schedules that are predictable so that they can budget for them appropriately. This is why many businesses prefer to lock in fixed rates of financing for longer durations. This enables them to have the minimum debt payment every month at a regular schedule that they can plan for.

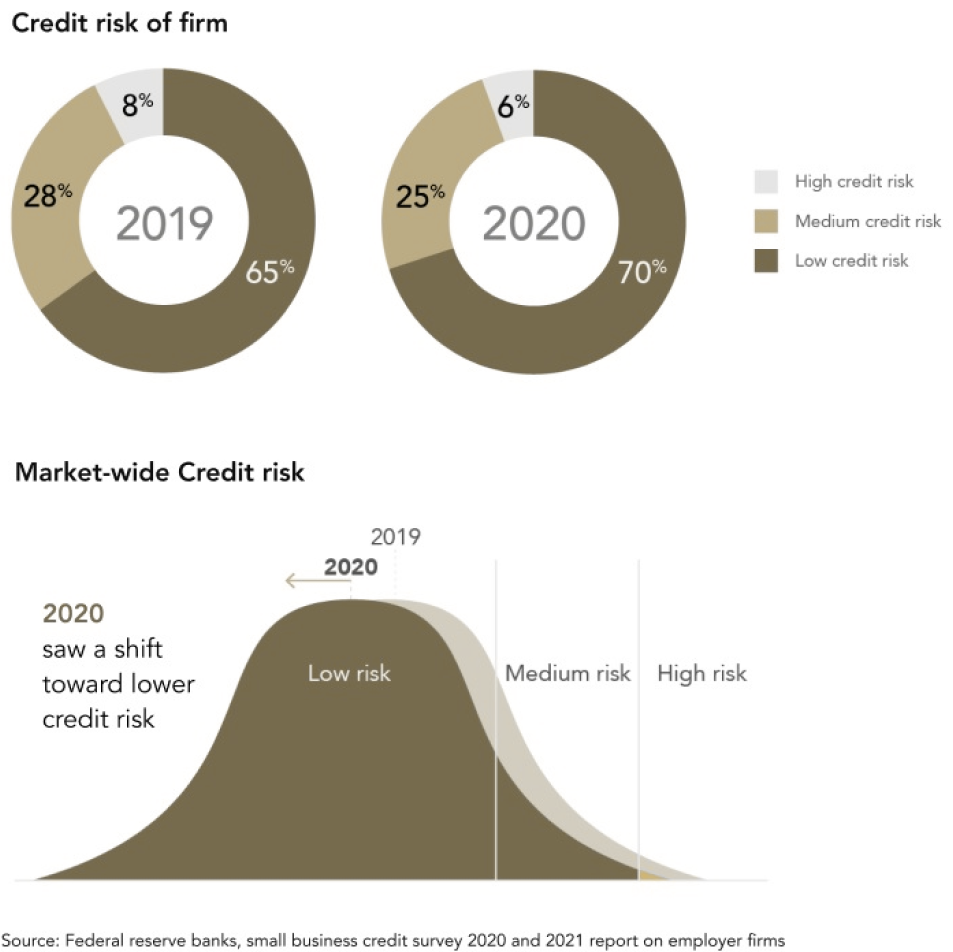

Are business too risky to lend to?

A key concern in lending is the credit risk profile of the business seeking capital. Risk is always present, but it ranges from low to high. Low-risk companies have a low probability of default. In other words, in aggregate, these businesses are more likely to pay their loan back. Conversely, high-risk businesses have a high likelihood of default. As a result, a lender faces a high probability that they will not pay back the full amount of the loan on time.

Businesses have been seeing greater access to credit. Pre-COVID, about 65% of businesses were considered “low” credit risks. Post COVID, this percentage has risen; around 70% of businesses are now low credit risk. This is a counterintuitive finding! After all, the pandemic had a negative impact on the economy – didn’t it.

One explanation is that the COVID-related economic downturn wiped out a lot of high-risk businesses. Thus, in aggregate, the businesses that made it through the COVID lockdowns were of better quality and hence lower credit risks. As a result, now is the best time in years for lenders to begin offering access to capital to growing businesses.If you are a software business that serves and aggregate s businesses, lending should be top of mind for you because it is top of mind for your users.

If you’re interested in understanding more about offering capital opportunities to some of your business customers, check in for more updates.

If you are a software business that serves and aggregates businesses, lending should be top of mind for you.

It is top of mind for your users.

Kanmon is operated by Kanmon Inc. Kanmon Inc makes capital available to businesses through business loans, lines of credit, and advances. California loans are made pursuant to Kanmon’s California Department of Financial Protection and Innovation (DFPI) Finance Lenders Law License #60DBO-144925. Kanmon does not currently meet the applicability thresholds for the California Consumer Privacy Act. As set forth in our Privacy Policy and with respect of California residents, Kanmon will not share information we collect about you with affiliated or non-affiliated third parties, except in the limited circumstances disclosed in our Privacy Policy and permitted under California law, or if you give us permission. To learn more, please contact hello@kanmon.com.